Quarterly Market Commentary - Autumn Outlook

The following document provides Quarterly Market Commentary for the forth quarter of 2020. This information is from FE Research.

Quarterly Market Commentary - Autumn Outlook

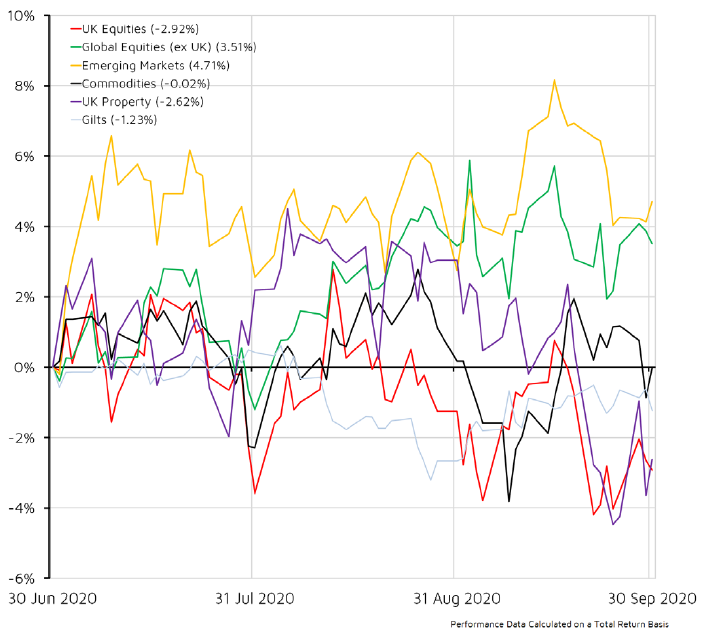

Review of the past quarter

Although the spread of coronavirus remained a concern, global financial markets continued their recovery. Investor sentiment favoured riskier assets and global equity markets produced the best performance. The strength of the recovery since the sell-off in March has seen several equity markets reaching new all-time highs in the last three months. Emerging market equities were the best performing region overall, although this hides big regional variations as Latin America and Europe, the Middle East and Africa (EMEA) continue to lag Asian markets. North American equities also continued their strong performance since the end of the sell-off in March. The recovery in emerging markets and the US has been driven by very strong performance in a small number of technology stocks. After such strong gains, the values of these companies fell in the first half of September as investors took some profits amid an increasingly uncertain outlook for economic recovery.

The UK continued to lag other developed economies and the FTSE All Share underperformed most other equity markets. The UK has experienced a bigger fall in economic activity than comparable countries and the return of Brexit as a political issue has dampened investor enthusiasm. The lack of progress over Brexit negotiations caused UK sterling to fall in value.

After a strong second quarter, higher quality government and corporate bonds have lagged behind most equity markets. Following their swift and decisive intervention in March and April, central banks have largely held off any further action.

The actuarial view:

Circumstances remain very challenging. After recent underperformance, expectations that UK equities will close the gap are receding. Strong recent performance from European equities reflects economic recovery and the prospect of resumption of trade with other improving economies. However, the recovery is still in its early stages and does herald a big increase in relative attractiveness.

US equities include some remarkable performers but also must contend with a resurgence of the virus and questions about whether valuations can be maintained. Japan and several other Asian economies have been spared the worst effect of the coronavirus, but markets were very quick to realise this and much of the benefit was absorbed into prices before the quarter began. The result is little relative change in outlook despite some evidence of improving economies.Lower rates make bond returns even more unbalanced towards the downside in the short term. UK rates moved more than other markets, reducing their attraction for investors. Corporate bonds suffer from increased uncertainty about the credit outlook. Property remains difficult, with very severe problems in a number of sectors.

WHAT TO LOOK FOR IN THE NEXT QUARTER:

- UK: The Monetary Policy Committee (MPC) announcements and minutes are set to be released on 5 November. Office for National Statistics update on economic effect of coronavirus on 8 October. Preliminary GDP growth for Q3 is available on 12 November. Daily number of new coronavirus cases.

- US: Presidential and congressional elections will be held on 3 November. There will be interest rate decisions from the Federal Open Market Committee (FOMC) on 4-5 November and 15-16 December. Minutes will be published three weeks after each decision. GDP growth for Q3 to be released on 25 November.

- Eurozone: Quarterly GDP flash data is set to published on 30 October. European Central Bank monetary policy meetings due on 29 October and 10 December. First estimate on Q3 GDP growth is due on 30 October and Q3 employment data is due on 13 November.

- Other Data: The next interest rate meeting from the Bank of Japan is on 28-29 October and next Opec meeting is on 30 November. The JPMorgan Global Composite PMI data is set to be published on 5 October.

ASSET CLASS SCENARIOS:

UK EQUITY

Most Likely: Fiscal and monetary measures are still expected to remain accommodative and lockdown measures to be less stringent than before. However, rising Brexit risk and increasing Covid-19 cases will continue to drive the underperformance of UK equities relative to their global peers as well as adversely impact UK sterling. With economic weakness remaining and little chance of inflation picking up, the performance baton is unlikely to move from growth stocks to value.

Worst Case: Reinstating full-scale lockdown measures, even for a shorter duration than March, will strongly impact the economy, irrespective of the level of stimulus package provided in response. A no-deal Brexit will also negatively affect all UK equities and send UK sterling falling, impacting domestically orientated smaller companies the most. A combination of a prolonged full lockdown and a no deal would be the worst scenario for UK equities.

Best Case: The surprise introduction of a working vaccine this year combined with at least some sort of a Brexit deal should remove the lid on performance, subsequently closing the premium gap to global peers. Strengthening UK sterling should mean domestically orientated small caps being the biggest winners, leaving large caps suffering on the margin from UK sterling appreciation.

CASH

Most Likely: The Bank of England has cut its interest rates to historic lows but is now contemplating a negative-rate policy by end of the year. Expectations have therefore worsened for cash investors. However, cash is likely to remain popular amongst market participants as volatility stays high. Money market funds will remain in demand for their liquidity features.

Worst Case: Although investors only expect the Bank of England to discuss negative rates, a move to negative rates can happen if the economic situation worsens. The return from money market funds will significantly drop, pushing investors into risky assets, while volatility is here to stay.

Best Case: A steady recovery would incentivise the Bank of England to maintain interest rates at current levels. This would see the return from cash slightly improve while inflation is well contained. Market participants would also remain more cautious in taking risk back, such that demand for cash and liquidity stays high.

GLOBAL EQUITY

Most Likely: The US election is on 3 November but we may have to wait for a result. Trump says he may contest a Democratic win, which could see further delay and increased volatility. In Europe coronavirus cases are increasing; however, monetary and fiscal policy remain supportive. Japanese prime minister Shinzo Abe’s resignation should be simpler as his right-hand man, Yoshihide Suga, is taking over, ensuring a continuation of ‘Abenomics’.

Worst Case: A Democrat White House, Senate and House of Representatives would make a corporate tax hike more likely. Democrat Joe Biden’s lead does not seem to have been priced in meaning equities could take a hit if he wins. Across Europe spending may drop the effects of a second wave of Covid-19 are felt.

Best Case: Central banks remain supportive, propping up markets and helping businesses. Low inflation and low rates could see equities make further gains, but as economic activity falls, and governments try to balance public health against the economy, some businesses will suffer. Unemployment benefits in the US have been reduced and further fiscal stimulus appears to be a way off, meaning the consumer driven US economy could contract further.

EMERGING MARKET EQUITY

Most Likely: An increase in volatility is likely heading in to the fourth quarter. Dispersion between countries should continue given Covid-19 cases are peaking in some, such as India, while tailing off in others with life returning to normal, like in North Asia. We expect China to continue its dominance as the demand side of its economy catches up with strong momentum on the supply side.

Worst Case: Further US-China trade uncertainty hasn’t been fully priced in, which has the potential to surprise to the downside. Uncertainty may linger regardless of who wins the US election. Biden would likely be more multilateralist in his approach to China, but neither may change the outcome of US-China relations, only the speed. The

weak spots are Latin America and India, where Covid-19 cases are sharply rising.

Best Case: The US presidential election could see US dollar weakness leading to some near-term relief. However, US dollar weakness alone would not be enough for a sharp rerating. The recent past has shown emerging markets underperformed relative to developed markets despite a weaker US dollar. A combination of Covid-19 cases under control across countries and a constructive development on US-China trade are needed to improve the outlook.

FIXED INCOME

Most Likely: Continued accommodative central bank policy should be expected to keep government bond yields low and within a tight range. Off the back of the notable rally in investment grade and high yield bonds, corporate bond valuations will likely hold steady, with most return generated from coupon income.

Worst Case: Developed governments signal earlier unwinding of fiscal stimulus and furlough packages than expected, meaning high yield bond defaults and losses would likely pick up beyond current expectations. In addition, any indication from a major central bank that it is considering straying from a ‘lower for longer’ interest rate strategy could trigger a significant sell-off across fixed income assets.

Best Case: Fixed income asset momentum continues as the Bank of England demonstrates a greater willingness to adopt negative rates, pushing gilt and investment grade valuations higher while encouraging more inflows into the high yield market as investors hunt for yield. Moreover, a slowdown in corporate bond issuance from historic levels in the first half of the year limits supply and pushes valuations higher.

PROPERTY

Most Likely: Significant US job losses will continue to hamper demand, whilst the hospitality and leisure industry are extremely vulnerable to any further restrictions following a second wave of Covid-19. We are likely to see ‘new world’ assets such as towers and data centres continue to outperform physical retail and leisure industry assets, with the potential for more payment holidays for tenants, dividend cuts and bankruptcies.

Worst Case: Localised attempts to halt the spread of Covid-19 fail and governments are forced to implement new nationwide lockdowns. If central banks and governments do not back this up with favourable monetary and fiscal policy – especially in the US where decision making is hampered by the upcoming election – then we could see the

return of the market stress seen in March.

Best Case: The new approach to containing coronavirus proves effective at shielding the vulnerable whilst letting most of the working population continue to move freely whilst improvements in treatments for Covid-19, and other respiratory illnesses, improve to avoid any winter health crises. Good news surrounding a UK-EU trade deal and a smoother-than-expected US election season would also help investors’ confidence.

Contact Us

Get in touch today

Call us, email, drop in, or fill in the form so that one of our expert advisers can be in touch.

We look forward to hearing from you and being your financial partner.

Guildford Office:

The Estate Yard

East Shalford Lane

Guildford

Surrey

GU4 8AE

London Office: c/o The Ministry, 79-81 Borough Rd, London, SE1 1DN